Consolidation Breakout PRO — Clean Boxes + 200 EMA Trend Filter High-probability range breakout detector that draws perfect, always-visible consolidation boxes and only alerts when price breaks out with strong volume and (optionally) in the direction of the prevailing trend.

Features

Automatically draws and extends clean consolidation boxes in real time

Boxes stop extending the moment the breakout occurs — no more “ghost” lines

Optional but powerful 200 EMA trend filter (dramatically reduces false breakouts)

Stronger volume confirmation (default 1.8× the 20-period average, fully adjustable)

Auto-deletes old boxes so your chart stays perfectly clean even after hundreds of signals

Clear “BREAKOUT ↑” and “BREAKDOWN ↓” labels + ready-to-use alerts

Works on any market and any timeframe (best on 1H, 4H, Daily)

How to trade it (edge > 65 % when used correctly)

Wait for the labeled breakout candle to close

Enter on pullback/retest of the box edge (or on strong close + retest)

Stop-loss just outside the opposite side of the box

Take-profit: minimum 1:2, ideally measured move (box height added/subtracted) or trailing with the 20 EMA

This is the cleanest and most professional public consolidation breakout tool available in 2025 — no repainting, no lag, no chart clutter.

Created and continuously improved with love for the TradingView community.

Cari dalam skrip untuk "take profit"

Advanced Trading System - Volume Profile + BB + RSI + FVG + FibAdvanced Multi-Indicator Trading System with Volume Profile, Bollinger Bands, RSI, FVG & Fibonacci

Overview

This comprehensive trading indicator combines five powerful technical analysis tools into one unified system, designed to identify high-probability trading opportunities with precision entry and exit signals. The indicator integrates Volume Profile analysis, Bollinger Bands, RSI momentum, Fair Value Gaps (FVG), and Fibonacci retracement levels to provide traders with a complete market analysis framework.

Key Features

1. Volume Profile & Point of Control (POC)

Automatically calculates the Point of Control - the price level with the highest trading volume

Identifies Value Area High (VAH) and Value Area Low (VAL)

Updates dynamically based on customizable lookback periods

Helps identify key support and resistance zones where institutional traders are active

2. Bollinger Bands Integration

Standard 20-period Bollinger Bands with customizable multiplier

Identifies overbought and oversold conditions

Measures market volatility through band width

Signals generated when price approaches extreme levels

3. RSI Momentum Analysis

14-period Relative Strength Index with visual background coloring

Overbought (70) and oversold (30) threshold alerts

Integrated into buy/sell signal logic for confirmation

Real-time momentum tracking in info dashboard

4. Fair Value Gap (FVG) Detection

Automatically identifies bullish and bearish fair value gaps

Visual representation with colored boxes

Highlights imbalance zones where price may return

Used for high-probability entry confirmation

5. Fibonacci Retracement Levels

Auto-calculated based on recent swing high/low

Key levels: 23.6%, 38.2%, 50%, 61.8%, 78.6%

Perfect for identifying profit-taking zones

Dynamic lines that update with market movement

6. Smart Signal Generation

The indicator generates BUY and SELL signals based on multi-condition confluence:

BUY Signal Requirements:

Price near lower Bollinger Band

RSI in oversold territory (< 30)

High volume confirmation (optional)

Bullish FVG or POC alignment

SELL Signal Requirements:

Price near upper Bollinger Band

RSI in overbought territory (> 70)

High volume confirmation (optional)

Bearish FVG or POC alignment

7. Automated Take Profit Levels

Three dynamic profit targets: 1%, 2%, and 3%

Automatically calculated from entry price

Visual markers on chart

Individual alerts for each level

8. Comprehensive Alert System

The indicator includes 10+ alert types:

Buy signal alerts

Sell signal alerts

Take profit level alerts (TP1, TP2, TP3)

Fibonacci level cross alerts

RSI overbought/oversold alerts

Bullish/Bearish FVG detection alerts

9. Real-Time Info Dashboard

Live display of all key metrics

Color-coded for quick visual analysis

Shows RSI, BB Width, Volume ratio, POC, Fib levels

Current signal status (BUY/SELL/WAIT)

How to Use

Setup

Add the indicator to your chart

Adjust parameters based on your trading style and timeframe

Set up alerts by clicking "Create Alert" and selecting desired conditions

Recommended Timeframes

Scalping: 5m - 15m

Day Trading: 15m - 1H

Swing Trading: 4H - Daily

Parameter Customization

Volume Profile Settings:

Length: 100 (adjust for more/less historical data)

Rows: 24 (granularity of volume distribution)

Bollinger Bands:

Length: 20 (standard period)

Multiplier: 2.0 (adjust for tighter/wider bands)

RSI Settings:

Length: 14 (standard momentum period)

Overbought: 70

Oversold: 30

Fibonacci:

Lookback: 50 (swing high/low detection period)

Signal Settings:

Volume Filter: Enable/disable volume confirmation

Volume MA Length: 20 (for volume comparison)

Trading Strategy Examples

Strategy 1: Trend Reversal

Wait for BUY signal at lower Bollinger Band

Confirm with bullish FVG or POC support

Enter position

Take partial profits at Fib 38.2% and 50%

Exit remaining position at TP3 or SELL signal

Strategy 2: Breakout Confirmation

Monitor price approaching POC level

Wait for volume spike

Enter on signal confirmation with FVG alignment

Use Fibonacci levels for scaling out

Strategy 3: Range Trading

Identify POC as range midpoint

Buy at lower BB with oversold RSI

Sell at upper BB with overbought RSI

Use FVG zones for additional confirmation

Best Practices

✅ Do:

Use multiple timeframe analysis

Combine with price action analysis

Set stop losses below/above recent swing points

Scale out at Fibonacci levels

Wait for volume confirmation on signals

❌ Don't:

Trade every signal blindly

Ignore overall market context

Use on extremely low timeframes without testing

Neglect risk management

Trade during low liquidity periods

Risk Management

Always use stop losses

Risk no more than 1-2% per trade

Consider market conditions and volatility

Scale position sizes based on signal strength

Use the volume filter for additional confirmation

Technical Specifications

Pine Script Version: 6

Overlay: Yes (displays on main chart)

Max Boxes: 500 (for FVG visualization)

Max Lines: 500 (for Fibonacci levels)

Alerts: 10+ customizable conditions

Performance Notes

This indicator works best in:

Trending markets with clear momentum

High-volume trading sessions

Assets with good liquidity

When multiple signals align

Less effective in:

Extremely choppy/sideways markets

Low-volume periods

During major news events (high volatility)

Updates & Support

This indicator is actively maintained and updated. Future enhancements may include:

Additional volume profile features

More sophisticated FVG tracking

Enhanced alert customization

Backtesting integration

Disclaimer

This indicator is for educational and informational purposes only. It does not constitute financial advice. Past performance does not guarantee future results. Always conduct your own research and consider consulting with a financial advisor before making trading decisions. Trading involves substantial risk of loss.

Low Volatility Breakout + TP/SL Levels█ OVERVIEW

"Low Volatility Breakout + TP/SL Levels" is a breakout indicator designed to detect and trade breakouts from periods of low volatility (consolidation). Unlike classic strategies based on fixed support/resistance levels, this indicator dynamically identifies consolidations characterized by small candle bodies and only generates a signal when the breakout occurs with a large, decisive candle. It also automatically plots 3 Take Profit levels and a Stop Loss (with two calculation modes), making it a complete breakout trading tool.

█ CONCEPTS

The strongest market moves most often start after a prolonged period of very low volatility — when candles become small and the market "falls asleep". The indicator first detects such consolidations (small bodies for at least X bars), draws a box around them, and then waits for a breakout with a candle significantly larger than the average. Additional filters (e.g., the box height cannot exceed the average candle body by too much) eliminate false consolidations and volatility traps. Immediately after the breakout, TP1, TP2, TP3, and SL levels are plotted.

█ FEATURES

Dynamic detection of low-volatility consolidations

- candles with small bodies (< average body × consolidationMultiplier)

- minimum number of bars in consolidation: confirmBars (default 5)

Automatic drawing of consolidation boxes

- green (bullish) or red (bearish) with transparent background (85)

- adjustable border thickness (border_width 1–5)

- box height filter (boxHeightMultiplier, default 6.0 × average body) – removes overly stretched/false consolidations

Breakout conditions

- current candle must be larger than average body × threshold (default 1.5)

- must be the largest candle in the entire consolidation

- must close above the highest high (long) or below the lowest low (short)

Breakout signals

- small green triangles below the bar (long)

- small red triangles above the bar (short)

Automatic Take Profit and Stop Loss levels (drawn 5 bars forward)

- two calculation modes:

• Candle Multiplier – based on average true range (high-low) over tp_sl_length period

• Percentage – fixed percentage from breakout close price (percentages must be manually adjusted to the asset and timeframe)

- 3 TP levels (default 2×, 3×, 4× or 2%, 3%, 4%)

- 1 SL level (default 2× or 1.5%)

Live TP/SL price table (top-right corner)

- displays exact current values of SL, TP1, TP2, TP3 immediately after each new signal

- colors identical to drawn lines (red background for SL, green for TP levels)

- updates automatically with every new breakout

Built-in alerts

- “Bullish Breakout Alert” and “Bearish Breakout Alert”

█ HOW TO USE

Add the indicator to your TradingView chart → Indicators → search “Low Volatility Breakout + TP/SL Levels”.

After each valid breakout you will immediately see:

- the colored box

- signal triangle

- horizontal TP/SL lines

- updated table in the top-right corner showing precise price levels for the current trade

Key settings to adjust:

Consolidation Settings

- Volatility Window (length) – period for average body calculation (default 20)

- Consolidation Multiplier – how small bodies must be to count as consolidation (default 2.0)

- Breakout Multiplier – minimum size of breakout candle (default 1.5)

- Box Height Multiplier – maximum allowed box height (default 6.0)

- Min Consolidation Bars – minimum bars required (default 5)

Risk Management Settings

- Choose TP/SL mode: Candle Multiplier or Percentage

- Adjust TP1–3 and SL multipliers/percentages to match your risk management style

Signal interpretation:

- Green triangle below bar + green box + green TP levels in table = long signal

- Red triangle above bar + red box + red SL level in table = short signal

- Boxes remain on chart until broken — they highlight accumulation/distribution zones

█ APPLICATIONS

- Trading breakouts from consolidation on all markets and timeframes

- Recommended to trade in the direction of the higher-timeframe trend or with additional confirmations (e.g., key level breaks). Aggressive mode (trading both directions) is also possible — provided box and TP/SL settings are properly optimized

- Experiment with different TP/SL ratios — higher reward-to-risk setups (e.g., SL 1×, TP3 6–8×) with lower win rate are often more profitable in the long run

- Strongly encourage testing various box parameters (consolidationMultiplier, boxHeightMultiplier, confirmBars) — small changes can dramatically affect signal frequency and quality

█ NOTES

Always test and optimize parameters for the specific instrument and timeframe.

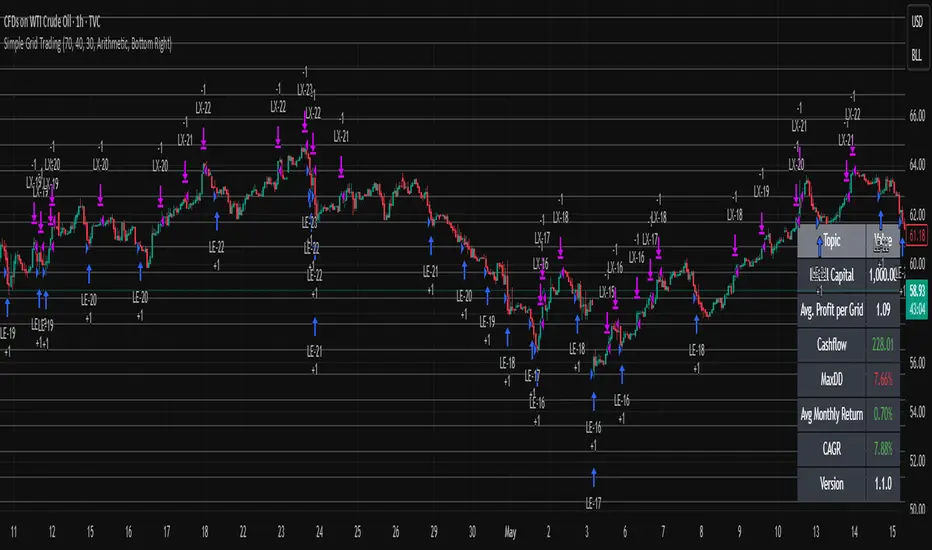

Simple Grid Trading v1.0 [PUCHON]Simple Grid Trading v1.0

Overview

This is a Long-Only Grid Trading Strategy developed in Pine Script v6 for TradingView. It is designed to profit from market volatility by placing a series of Buy Limit orders at predefined price levels. As the price drops, the strategy accumulates positions. As the price rises, it sells these positions at a profit.

Features

Grid Types : Supports both Arithmetic (equal price spacing) and Geometric (equal percentage spacing) grids.

Flexible Order Management : Uses strategy.order for precise control and prevents duplicate orders at the same level.

Performance Dashboard : A real-time table displaying key metrics like Capital, Cashflow, and Drawdown.

Advanced Metrics : Includes Max Drawdown (MaxDD) , Avg Monthly Return , and CAGR calculations.

Customizable : Fully adjustable price range, grid lines, and lot size.

Dashboard Metrics

The dashboard (default: Bottom Right) provides a quick snapshot of the strategy's performance:

Initial Capital : The starting capital defined in the strategy settings.

Lot Size : The fixed quantity of assets purchased per grid level.

Avg. Profit per Grid : The average realized profit for each closed trade.

Cashflow : The total realized net profit (closed trades only).

MaxDD : Maximum Drawdown . The largest percentage drop in equity (realized + unrealized) from a peak.

Avg Monthly Return : The average percentage return generated per month.

CAGR : Compound Annual Growth Rate . The mean annual growth rate of the investment over the specified time period.

Strategy Settings (Inputs)

Grid Settings

Upper Price : The highest price level for the grid.

Lower Price : The lowest price level for the grid.

Number of Grid Lines : The total number of levels (lines) in the grid.

Grid Type :

Arithmetic: Distance between lines is fixed in price terms (e.g., $10, $20, $30).

Geometric: Distance between lines is fixed in percentage terms (e.g., 1%, 2%, 3%).

Lot Size : The fixed amount of the asset to buy at each level.

Dashboard Settings

Show Dashboard : Toggle to hide/show the performance table.

Position : Choose where the dashboard appears on the chart (e.g., Bottom Right, Top Left).

How It Works

Initialization : On the first bar, the script calculates the price levels based on your Upper/Lower price and Grid Type.

Entry Logic :

The strategy places Buy Limit orders at every grid level below the current price.

It checks if a position already exists at a specific level to avoid "stacking" multiple orders on the same line.

Exit Logic :

For every Buy order, a corresponding Sell Limit (Take Profit) order is placed at the next higher grid level.

MaxDD Calculation :

The script continuously tracks the highest equity peak.

It calculates the drawdown on every bar (including intra-bar movements) to ensure accuracy.

Displayed as a percentage (e.g., 5.25%).

Disclaimer

This script is for educational and backtesting purposes only. Grid trading involves significant risk, especially in strong trending markets where the price may move outside your grid range. Always use proper risk management.

NIFTY Options Breakout StrategyThis strategy trades NIFTY 50 Options (CALL & PUT) using 5-minute breakout logic, strict trend filters, expiry-based symbol validation, and a dynamic trailing-profit engine.

1️⃣ Entry Logic

Only trades NIFTY 50 options, filtered automatically by symbol.

Trades only between 10:00 AM – 2:15 PM (5m bars).

Breakout trigger:

Price enters the buy breakout zone (high of last boxLookback bars ± buffer).

Trend filter:

Price must be above EMA50 or EMA200,

AND EMA50 ≥ EMA100 (to avoid weak conditions).

Optional strengthening:

EMA20>EMA50 OR EMA50>EMA100 recent cross can be enforced.

Higher-timeframe trend check:

EMA50 > EMA200 (bullish regime only).

Start trading options only after expiry–2 months (auto-parsed).

2️⃣ One Trade Per Day

Maximum 1 long trade per day.

No shorting (long-only strategy).

3️⃣ Risk Management — SL, TP & Trailing

Includes three types of exits:

🔹 A) Hard SL/TP

Hard Stop-Loss: -15%

Hard Take-Profit: +40%

🔹 B) Step-Ladder Trailing Profit

As the option price rises, trailing activates:

Max Profit Reached Exit Trigger When Falls To

≥ 35% ≤ 30%

≥ 30% ≤ 25%

≥ 25% ≤ 20%

≥ 20% ≤ 15%

≥ 15% ≤ 10%

≥ 5% ≤ 0%

🔹 C) Loss-Recovery Exit

If loss reaches –10% but then recovers to 0%, exit at breakeven.

4️⃣ Trend-Reversal Exit

If price closes below 5m EMA50, the long is exited instantly.

5️⃣ Optional Intraday Exit

EOD square-off at 3:15 PM.

6️⃣ Alerts for Automation

The strategy provides alerts for:

BUY entry

TP/SL/Trailing exit

EMA50 reversal exit

EOD exit

Market Energy & Direction DashboardMarket Energy & Direction Dashboard - Daytrading

Overview

A comprehensive real-time market internals dashboard that combines NYSE TICK, NYSE Advance-Decline (ADD) momentum, VIX direction, and relative volume into a single visual traffic light system with intelligent signal synthesis. Designed for active daytraders who need instant confirmation of market direction and energy based on momentum alignment across all major internals.

What It Does

This indicator synthesizes multiple market internals using directional momentum analysis rather than static thresholds to provide clear, actionable signals:

• Traffic Light System: Single glance confirmation of market state

o Bright Green: Maximum bullish - all internals aligned (TICK + ADD rising + VIX falling + volume)

o Bright Red: Maximum bearish - all internals aligned (TICK + ADD falling + VIX rising + volume)

o Yellow: Exhaustion warning - TICK at extremes, potential reversal imminent

o Moderate Colors: Partial alignment - some confirmation but not complete

o Gray: Choppy, neutral, or conflicting signals

• Real-Time Dashboard displays:

o Current TICK value with exhaustion warnings

o Current ADD with directional momentum indicator (↑ rising = breadth improving, ↓ falling = breadth deteriorating, ± compression)

o VIX level with directional indicator (↓ declining = bullish, ↑ rising = bearish, ± compression = neutral)

o Relative volume (current vs 20-period average)

o Composite status message synthesizing all data into clear directional summary

Key Features

✓ Momentum-based analysis - all indicators show direction/change, not just levels ✓ Intelligent signal hierarchy from "Maximum" to "Moderate" based on internal alignment ✓ ADD directional momentum - catches breadth shifts early, works in all market conditions ✓ VIX directional analysis - shows if fear is increasing, decreasing, or stagnant ✓ Color-coded traffic light for instant decision making ✓ Detects TICK/ADD divergences (conflicting signals = caution) ✓ Exhaustion warnings at extreme TICK levels (±1000+) ✓ Composite status messages - "Maximum Bull", "Strong Bull", "Moderate Bull", etc. ✓ Customizable thresholds for all parameters ✓ Moveable dashboard (9 position options) ✓ Built-in alerts for all signal strengths, exhaustion, and divergences

How To Use

Setup:

1. Add indicator to your main trading chart (SPY, ES, NQ, etc.)

2. Default settings work well for most traders, but you can customize:

o TICK Extreme Level (default 1000)

o ADD Compression Threshold (default 100 - detects when breadth is stagnant)

o VIX Elevated Level (default 20)

o VIX Compression Threshold (default 2% - detects low volatility)

o Volume Threshold (default 1.5x average)

3. Position dashboard wherever convenient on your chart

Reading The Signals:

Signal Hierarchy (Strongest to Weakest):

MAXIMUM SIGNALS ⭐ (Brightest colors - All 4 internals aligned)

• "✓ MAXIMUM BULL": TICK bullish + ADD rising (↑) + VIX falling (↓) + Volume elevated

o This is the holy grail setup - all momentum aligned, highest conviction longs

• "✓ MAXIMUM BEAR": TICK bearish + ADD falling (↓) + VIX rising (↑) + Volume elevated

o Perfect storm bearish - all momentum aligned, highest conviction shorts

STRONG SIGNALS (Bright colors - Core internals aligned)

• "✓ STRONG BULL": TICK bullish + ADD rising (↑)

o Strong confirmation even without VIX/volume - breadth supporting the move

• "✓ STRONG BEAR": TICK bearish + ADD falling (↓)

o Strong confirmation - both momentum and breadth deteriorating

MODERATE SIGNALS (Faded colors - Partial confirmation)

• "MODERATE BULL": TICK bullish but ADD not confirming direction

o Proceed with caution - momentum present but breadth questionable

• "MODERATE BEAR": TICK bearish but ADD not confirming direction

o Proceed with caution - selling but breadth not fully participating

WARNING SIGNALS

• "⚠ EXHAUSTION" (Yellow): TICK at ±1000+ extremes

o Potential reversal zone - prepare to fade or take profits

o Often marks blow-off tops or capitulation bottoms

NEUTRAL/AVOID

• "CHOPPY/NEUTRAL" (Gray): Conflicting signals or low conviction

o Stay out or reduce size significantly

Individual Indicator Interpretation:

TICK:

• Green: Bullish momentum (>+300)

• Red: Bearish momentum (<-300)

• Yellow: Exhaustion (±1000+)

• Gray: Neutral

ADD (Advance-Decline):

• Green (↑): Breadth improving - more stocks participating in the move

• Red (↓): Breadth deteriorating - fewer stocks participating

• Gray (±): Breadth stagnant - no clear participation trend

VIX:

• Green (↓): Fear declining - healthy environment for rallies

• Red (↑): Fear rising - risk-off mode, supports downward moves

• Gray (±): Volatility compression - often precedes explosive moves

Volume:

• Green: High conviction (>1.5x average)

• Gray: Low conviction

Trading Strategy:

1. Wait for "MAXIMUM" or "STRONG" signals for highest probability entries

o Maximum signals = go full size with confidence

o Strong signals = good conviction, normal position sizing

2. Confirm directional alignment:

o For longs: Want ADD ↑ (rising) and VIX ↓ (falling)

o For shorts: Want ADD ↓ (falling) and VIX ↑ (rising)

3. Use exhaustion warnings (yellow) to:

o Take profits on existing positions

o Prepare counter-trend entries

o Tighten stops

4. Avoid "MODERATE" signals unless you have strong conviction from other analysis

o These work best as confirmation for existing setups

o Not strong enough to initiate new positions alone

5. Never trade "CHOPPY/NEUTRAL" signals

o Gray means stay out - preserve capital

o Wait for clear alignment

6. Watch for divergences:

o Price making new highs but ADD ↓ (falling) = distribution warning

o Price making new lows but ADD ↑ (rising) = potential bottom

o Divergence alert will notify you

Best Practices:

• Use on 1-5 minute charts for daytrading

• Combine with your price action or technical setup (support/resistance, trendlines, patterns)

• The dashboard confirms when to take your setup, not what setup to take

• Most effective during regular market hours (9:30 AM - 4:00 PM ET) when volume is present

• The strongest edge comes from "MAXIMUM" signals - wait for these for best risk/reward

• Pay special attention to ADD direction - it's the most predictive breadth indicator

• VIX compression (gray ±) often signals upcoming volatility expansion - prepare for bigger moves

Customization Option

All thresholds are adjustable in settings:

• TICK Extreme: Higher = fewer exhaustion warnings (try 1200-1500 for less sensitivity)

• ADD Compression Threshold: Change detection sensitivity

o Default 100 = balanced

o Lower (50) = more sensitive to small breadth changes

o Higher (200-300) = only shows major breadth shifts

• VIX Elevated: Adjust for current volatility regime (15-25 typical range)

• VIX Compression Threshold:

o Default 2% = balanced

o Lower (0.5-1%) = catches subtle VIX changes

o Higher (3-5%) = only shows significant VIX moves

• Volume Threshold: Lower for quieter stocks/times, higher for more confirmation

Alerts Available

• Maximum Bullish: All 4 internals aligned bullish (TICK + ADD↑ + VIX↓ + Volume)

• Maximum Bearish: All 4 internals aligned bearish (TICK + ADD↓ + VIX↑ + Volume)

• Strong Bullish: TICK bullish + ADD rising

• Strong Bearish: TICK bearish + ADD falling

• Exhaustion Warning: TICK at extreme levels

• Divergence Warning: TICK and ADD directions conflicting

Understanding the Signal Synthesis

The indicator uses intelligent logic to combine all internals:

"MAXIMUM" Signals require:

• TICK direction (bullish/bearish)

• ADD momentum (rising/falling) in same direction

• VIX direction (falling for bulls, rising for bears)

• Volume elevated (>1.5x average)

"STRONG" Signals require:

• TICK direction (bullish/bearish)

• ADD momentum (rising/falling) in same direction

• (VIX and volume are bonuses but not required)

"MODERATE" Signals:

• TICK showing direction

• But ADD not confirming or contradicting

• Weakest actionable signal

This hierarchy ensures you know exactly how much conviction the market has behind any move.

Technical Details

• Pulls real-time data from NYSE TICK (USI:TICK), NYSE ADD (USI:ADD), and CBOE VIX

• ADD direction calculated using bar-to-bar change with compression detection

• VIX direction calculated using bar-to-bar percentage change

• Volume calculation uses 20-period simple moving average

• Dashboard updates every bar

• No repainting - all calculations based on closed bar data

Who This Is For

• Active daytraders of stocks, futures (ES/NQ), and options

• Scalpers needing quick directional confirmation with multiple internal alignment

• Swing traders looking to time intraday entries with maximum confluence

• Volatility traders who monitor VIX behavior

• Market makers and professionals who trade based on breadth and internals

• Anyone who monitors market internals but wants intelligent synthesis vs raw data

Tips For Success

Trading Philosophy:

• Quality over quantity - wait for "MAXIMUM" signals for best results

• One "MAXIMUM" signal trade is worth five "MODERATE" signal trades

• Gray/neutral is not a sign of missing opportunity - it's protecting your capital

Signal Confidence Levels:

1. MAXIMUM (95%+ confidence) - Trade these aggressively with full size

2. STRONG (80-85% confidence) - Trade these with normal position sizing

3. MODERATE (60-70% confidence) - Only if confirmed by strong technical setup

4. CHOPPY/NEUTRAL - Do not trade, wait for clarity

Advanced Techniques:

• Breadth divergences: Watch for price making new highs while ADD shows ↓ (falling) = major warning

• VIX/Price divergences: Rallies with rising VIX (↑) are usually false moves

• Volume confirmation: "MAXIMUM" signals with 2x+ volume are the absolute best

• Compression zones: When both ADD and VIX show compression (±), expect explosive breakout soon

• Sequential signals: Back-to-back "MAXIMUM" signals in same direction = strong trending day

Common Patterns:

• Opening surge with "MAXIMUM BULL" that shifts to "EXHAUSTION" (yellow) = fade the high

• Selloff with "MAXIMUM BEAR" followed by ADD ↑ (rising) divergence = potential reversal

• Choppy morning followed by "MAXIMUM" signal afternoon = best trending opportunity

Example Scenarios

Perfect Bull Entry:

• Bright green signal box

• TICK: +650

• ADD: +1200 (↑)

• VIX: 18.30 (↓)

• Volume: 2.3x

• Status: "✓ MAXIMUM BULL" → ALL SYSTEMS GO - Take aggressive long positions

Strong Bull (Good Confidence):

• Green signal box (slightly less bright)

• TICK: +500

• ADD: +800 (↑)

• VIX: 19.50 (±)

• Volume: 1.2x

• Status: "✓ STRONG BULL" → Good long setup - breadth confirming even without VIX/volume

Caution Bull (Moderate):

• Faded green signal box

• TICK: +400

• ADD: +900 (↓)

• VIX: 20.10 (↑)

• Volume: 0.9x

• Status: "MODERATE BULL" → CAUTION - TICK bullish but breadth deteriorating and VIX rising = weak rally

Exhaustion Warning:

• Yellow signal box

• TICK: +1350 ⚠

• ADD: +2100 (↑)

• VIX: 17.20 (↓)

• Volume: 1.8x

• Status: "⚠ EXHAUSTION" → Take profits or prepare to fade - TICK overextended despite good internals

Divergence Setup (Potential Reversal):

• Faded green signal

• TICK: +300

• ADD: +1800 (↓)

• VIX: 21.50 (↑)

• Volume: 1.6x

• Status: "MODERATE BULL" → WARNING - Price rallying but breadth collapsing and fear rising = distribution

Perfect Bear Entry:

• Bright red signal box

• TICK: -780

• ADD: -1600 (↓)

• VIX: 24.80 (↑)

• Volume: 2.5x

• Status: "✓ MAXIMUM BEAR" → Perfect short setup - all momentum bearish with conviction

Compression (Wait Mode):

• Gray signal box

• TICK: +50

• ADD: -200 (±)

• VIX: 16.40 (±)

• Volume: 0.7x

• Status: "CHOPPY/NEUTRAL" → STAY OUT - Volatility compression, no conviction, await breakout

Performance Optimization

Best Market Conditions:

• Works excellent in trending markets (up or down)

• Particularly powerful during high-volume sessions (first/last hours)

• "MAXIMUM" signals most reliable during 9:45-11:00 AM and 2:00-3:30 PM ET

Less Effective During:

• Lunch period (11:30 AM - 1:30 PM) - lower volume reduces signal quality

• Low-volatility environments - compression signals dominate

• Major news events in first 5 minutes - wait for internals to stabilize

Recommended Use Cases:

• Scalping: Trade only "MAXIMUM" signals for quick 5-15 minute moves

• Daytrading: Use "MAXIMUM" and "STRONG" signals for position entries

• Swing entries: Use "MAXIMUM" signals for optimal intraday entry timing

• Exit timing: Use "EXHAUSTION" (yellow) warnings to take profits

________________________________________

Pro Tip: Create a dedicated workspace with this indicator on SPY/ES/NQ charts. Set alerts for "MAXIMUM BULL", "MAXIMUM BEAR", and "EXHAUSTION" signals. Most professional traders only trade the "MAXIMUM" setups and ignore everything else - this alone can dramatically improve win rates.

DEMA ATR Strategy [PrimeAutomation]⯁ OVERVIEW

The DEMA ATR Strategy combines trend-following logic with adaptive volatility filters to identify strong momentum phases and manage trades dynamically.

It uses a Double Exponential Moving Average (DEMA) anchored to ATR volatility bands, creating a self-adjusting trend baseline.

When the adjusted DEMA shifts direction, the strategy enters positions and scales out profit in phases based on ATR-driven targets.

This system adapts to volatility, filters noise, and seeks sustained directional moves.

⯁ KEY FEATURES

DEMA-Volatility Hybrid Filter

Uses Double EMA with ATR expansion/compression logic to form a dynamic trend baseline.

Directional Shift Entries

Entries occur when the adjusted DEMA flips trend (bullish crossover or bearish crossunder vs its past value).

Noise Reduction Mechanism

ATR range caps extreme moves and prevents false flips during choppy volatility spikes.

Multi-Level Take Profits

Targets scale out positions at 1×, 2×, and 3× ATR multiples in the trade direction.

Volatility-Adaptive Targets

ATR multiplier ensures profit targets expand/contract based on market conditions.

Single-Direction Exposure

No pyramiding; the strategy flips position only when trend shifts.

Automated Trade Finalization

When all profit targets trigger, the position is fully closed.

⯁ STRATEGY LOGIC

Trend Direction:

DEMA baseline is modified using ATR upper/lower envelopes.

• If the adjusted DEMA rises above previous value → Bullish

• If it falls below previous value → Bearish

Entry Rules:

• Enter Long when bullish shift occurs and no long position exists

• Enter Short when bearish shift occurs and no short position exists

Take Profit Logic:

3 partial exits for each trade based on ATR:

• TP1 = ±1× ATR

• TP2 = ±2× ATR

• TP3 = ±3× ATR

Profit distribution: 30% / 30% / 40%

Exit Conditions:

• Exit when all TPs hit (full scale-out if sum of all TPs 100%)

• Opposite trend signal closes current trade and opens new one

⯁ WHEN TO USE

Trending environments

Medium–high volatility phases

Swing trading and intraday trend plays

Markets that respect momentum continuation (crypto, indices, FX majors)

⯁ CONCLUSION

This strategy blends DEMA trend recognition with ATR-based volatility adaptation to generate cleaner directional entries and structured take-profit exits. It is designed to capture momentum phases while avoiding noise-driven false signals, delivering a disciplined and scalable trend-following approach.

Crypto Grid 2025+ Long Only (Asym TP)Crypto Grid 2025+ Long Only (Asymmetric Take-Profit) is a long-only mean-reversion grid strategy designed for intraday cryptocurrency trading.

The core idea is to accumulate long positions as price moves downward within a locally defined price range and to exit positions on upward retracements.

The strategy automatically builds a multi-level grid between the highest and lowest price over a user-defined lookback period (“range length”). Each grid level acts as a potential entry point when price crosses it from above.

Key Features

1. Long-only grid logic

The strategy opens long positions only, progressively increasing exposure as price moves into lower grid levels.

2. Asymmetric take-profit mechanism

Instead of taking profit strictly at the next grid level, the strategy allows targeting multiple levels above the entry point. This increases the average profit per winning trade and shifts the reward-to-risk profile toward larger, less frequent wins.

3. Optional partial take-profit

A portion of each trade can be closed at the nearest grid level, while the remainder is held for a more distant asymmetric target. This balances consistency and profit potential.

4. Volume-based market filter

Entries can be restricted to periods of healthy market activity by requiring volume to exceed a moving-average baseline.

5. Capital-scaled position sizing

Position size is determined by risk percentage, grid spacing, and a dynamic sizing mode (original / conservative / aggressive).

6. Built-in risk controls

global stop below the lower boundary of the range,

global take-profit above the upper boundary,

automatic shutdown after a configurable loss-streak.

Market Philosophy

This strategy belongs to the mean-reversion family: it expects short-term overshoots to revert back toward mid-range liquidity zones.

It is not trend-following.

It performs best in choppy, range-bound, or slow-grinding markets — especially on liquid crypto pairs.

Recommended Use Cases

Short timeframes (1–15 minutes)

High-liquidity crypto pairs

Sideways or rotational price action

Exchanges with low fees (due to higher order count)

Not Intended For

Strong trending markets without pullbacks

Assets with thin order books

Use with leverage without additional risk controls

Summary

Crypto Grid 2025+ Long Only (Asymmetric TP) is a refined grid-based mean-reversion strategy optimized for modern crypto markets. Its asymmetric take-profit framework is specifically engineered to reduce the classical issue of “small wins and large occasional losses” found in traditional grid systems, giving it a more favorable long-term trade distribution.

PivotBoss VWAP Bands (Auto TF) - FixedWhat this indicator shows (high level)

The indicator plots a VWAP line and three bands above (R1, R2, R3) and three bands below (S1, S2, S3).

Band spacing is computed from STD(abs(VWAP − price), N) and multiplied by 1, 2 and 3 to form R1–R3 / S1–S3. The script is timeframe-aware: on 30m/1H charts it uses Weekly VWAP and weekly bands; on Daily charts it uses Monthly VWAP and monthly bands; otherwise it uses the session/chart VWAP.

VWAP = the market’s volume-weighted average price (a measure of fair value). Bands = volatility-scaled zones around that fair value.

Trading idea — concept summary

VWAP = fair value. Price above VWAP implies bullish bias; below VWAP implies bearish bias.

Bands = graded overbought/oversold zones. R1/S1 are near-term limits, R2/S2 are stronger, R3/S3 are extreme.

Use trend alignment + price action + volume to choose higher-probability trades. VWAP bands give location and magnitude; confirmations reduce false signals.

Entry rules (multiple strategies with examples)

A. Momentum breakout (trend-following) — preferred on trending markets

Setup: Price consolidates near or below R1 and then closes above R1 with above-average volume. Chart: 30m/1H (Weekly VWAP) or Daily (Monthly VWAP) depending on your timeframe.

Entry: Enter long at the close of the breakout bar that closes above R1.

Stop-loss: Place initial stop below the higher of (VWAP or recent swing low). Example: if price broke R1 at ₹1,200 and VWAP = ₹1,150, set stop at ₹1,145 (5 rupee buffer below VWAP) or below the last swing low if that is wider.

Target: Partial target at R2, full target at R3. Trail stop to VWAP or to R1 after price reaches R2.

Example numeric: Weekly VWAP = ₹1,150, R1 = ₹1,200, R2 = ₹1,260. Buy at ₹1,205 (close above R1), stop ₹1,145, target1 ₹1,260 (R2), target2 ₹1,320 (R3).

B. Mean-reversion fade near bands — for range-bound markets

Setup: Market is not trending (VWAP flatish). Price rallies up to R2 or R3 and shows rejection (pin bar, bearish engulfing) on increasing or neutral volume.

Entry: Enter short after a confirmed rejection candle that fails to sustain above R2 or R3 (prefer confirmation: close back below R1 or below the rejection candle low).

Stop-loss: Just above the recent high (e.g., 1–2 ATR or a fixed buffer above R2/R3).

Target: First target VWAP, second target S1. Reduce size if taking R3 fade as it’s an extreme.

Example numeric: VWAP = ₹950, R2 = ₹1,020. Price spikes to ₹1,025 and forms a bearish engulfing candle. Enter short at ₹1,015 after the next close below ₹1,020. Stop at ₹1,035, target VWAP ₹950.

C. Pullback entries in trending markets — higher probability

Setup: Price is above VWAP and trending higher (higher highs and higher lows). Price pulls back toward VWAP or S1 with decreasing downside volume and a reversal candle forms.

Entry: Long when price forms a bullish reversal (hammer/inside-bar) with a close back above the pullback candle.

Stop-loss: Below the pullback low (or below S2 if a larger stop is justified).

Target: VWAP then R1; if momentum resumes, trail toward R2/R3.

Example numeric: Price trending above Weekly VWAP at ₹1,400; pullback to S1 at ₹1,360. Enter long at ₹1,370 when a bullish candle closes; stop at ₹1,350; first target VWAP ₹1,400, second target R1 ₹1,450.

Exit rules and money management

Basic exit hierarchy

Hard stop exit — when price hits initial stop-loss. Always use.

Target exit — take partial profits at R1/R2 (for longs) or S1/S2 (for shorts). Use trailing stops for the remainder.

VWAP invalidation — if you entered long above VWAP and price returns and closes significantly below VWAP, consider exiting (condition depends on timeframe and trade size).

Price action exit — reversal patterns (strong opposite candle, bearish/bullish engulfing) near targets or beyond signals to exit.

Trailing rules

After price reaches R2, move stop to breakeven + a small buffer or to VWAP.

After price reaches R3, trail by 1 ATR or lock a defined profit percentage.

Position sizing & risk

Risk per trade: commonly 0.5–2% of account equity.

Determine position size by RiskAmount ÷ (EntryPrice − StopPrice).

If the stop distance is large (e.g., trading R3 fades), reduce position size.

Filters & confirmation (to reduce false signals)

Volume filter: For breakouts, require volume above short-term average (e.g., >20-period average). Breakouts on low volume are suspect.

Trend filter: Only take breakouts in the direction of the higher-timeframe trend (for example, use Daily/Weekly trend when trading 30m/1H).

Candle confirmation: Prefer entries on close of the confirming candle (not intrabar noise).

Multiple confirmations: When R1 break happens but RSI/plotted momentum indicator does not confirm, treat signal as lower probability.

Special considerations for timeframe-aware logic

On 30m/1H the script uses Weekly VWAP/bands. That means band levels change only on weekly candles — they are strong, structural levels. Treat R1/R2/R3 as significant and expect fewer, stronger signals.

On Daily, the script uses Monthly VWAP/bands. These are wider; trades should allow larger stops and smaller position sizes (or be used for swing trades).

On other intraday charts you get session VWAP (useful for intraday scalps).

Example: If you trade 1H and the Weekly R1 is at ₹2,400 while session VWAP is ₹2,350, a close above Weekly R1 represents a weekly-level breakout — prefer that for swing entries rather than scalps.

Example trade walkthrough (step-by-step)

Context: 1H chart, auto-mapped → Weekly VWAP used.

Weekly VWAP = ₹3,000; R1 = ₹3,080; R2 = ₹3,150.

Price consolidates below R1. A large bullish candle closes at ₹3,085 with volume 40% above the 20-bar average.

Entry: Buy at close ₹3,085.

Stop: Place stop at ₹2,995 (just under Weekly VWAP). Risk = ₹90.

Position size: If risking ₹900 per trade → size = 900 ÷ 90 = 10 units.

Targets: Partial take-profit at R2 = ₹3,150; rest trailed with stop moved to breakeven after R2 is hit.

If price reverses and closes below VWAP within two bars, exit immediately to limit drawdown.

When to avoid trading these signals

High-impact news (earnings, macro announcements) that can gap through bands unpredictably.

Thin markets with low volume — VWAP loses significance when volumes are extremely low.

When weekly/monthly bands are flat but intraday price is volatile without clear structure — prefer session VWAP on smaller timeframes.

Alerts & automation suggestions

Alert on close above R1 / below S1 (use the built-in alertcondition the script adds). For higher-confidence alerts, require volume filter in the alert condition.

Automated order rules (if you automate): use limit entry at breakout close plus a small slippage buffer, immediate stop order, and OCO for TP and SL.

EMA Trend Pro v1Here is a clear, professional English description you can copy-paste directly (suitable for sharing with friends, investors, brokers, or posting on TradingView):

EMA Trend Pro v5.0 – Strategy Overview

This is a trend-following strategy designed for 15-minute charts on assets like XAUUSD, NASDAQ, BTC, and ETH.

Entry Rules

Buy when the 7, 14, and 21-period EMAs are aligned upward and the 14-period EMA crosses above the 144-period EMA (with ADX > 20 and volume confirmation).

Sell short when the EMAs are aligned downward and the 14-period EMA crosses below the 144-period EMA.

Risk Management

Initial stop-loss is placed at 1.8 × ATR below (long) or above (short) the entry price.

Position size is calculated to risk a fixed percentage of equity per trade.

Profit-Taking & Trade Management

When price reaches 1:1 reward-to-risk, 30% of the position is closed.

At the same moment, the stop-loss for the remaining 70% is moved to the entry price (breakeven).

The remaining position is split:

50% targets 1:2 reward-to-risk

50% targets 1:3 reward-to-risk (allowing big wins during strong trends)

Visualization

Clean colored bars extend to the right showing entry, stop-loss, and three take-profit levels.

Price labels clearly display "Entry", "SL", "TP1 1:1", "TP2 1:2", and "TP3 1:3".

Only the current trade is displayed for a clean chart.

Key Advantages

High win rate due to breakeven protection after 1R

Excellent reward-to-risk ratio that lets winners run

Fully automated, works on any market with clear trends

Professional look, easy to understand and explain

Perfect for swing traders who want consistent profits with limited downside risk.

Feel free to use this description on TradingView, in your trading journal, or when explaining the strategy to others!

If you want a shorter version (e.g., for TradingView description box) or a Chinese version, just let me know — I’ll give it to you right away! 😊

EMA Trend Pro v5.0 5M ONLY — 策略版(1:1出30%+保本)Here is a clear, professional English description you can copy-paste directly (suitable for sharing with friends, investors, brokers, or posting on TradingView):

EMA Trend Pro v5.0 – Strategy Overview

This is a trend-following strategy designed for 15-minute charts on assets like XAUUSD, NASDAQ, BTC, and ETH.

Entry Rules

Buy when the 7, 14, and 21-period EMAs are aligned upward and the 14-period EMA crosses above the 144-period EMA (with ADX > 20 and volume confirmation).

Sell short when the EMAs are aligned downward and the 14-period EMA crosses below the 144-period EMA.

Risk Management

Initial stop-loss is placed at 1.8 × ATR below (long) or above (short) the entry price.

Position size is calculated to risk a fixed percentage of equity per trade.

Profit-Taking & Trade Management

When price reaches 1:1 reward-to-risk, 30% of the position is closed.

At the same moment, the stop-loss for the remaining 70% is moved to the entry price (breakeven).

The remaining position is split:

50% targets 1:2 reward-to-risk

50% targets 1:3 reward-to-risk (allowing big wins during strong trends)

Visualization

Clean colored bars extend to the right showing entry, stop-loss, and three take-profit levels.

Price labels clearly display "Entry", "SL", "TP1 1:1", "TP2 1:2", and "TP3 1:3".

Only the current trade is displayed for a clean chart.

Key Advantages

High win rate due to breakeven protection after 1R

Excellent reward-to-risk ratio that lets winners run

Fully automated, works on any market with clear trends

Professional look, easy to understand and explain

Perfect for swing traders who want consistent profits with limited downside risk.

Feel free to use this description on TradingView, in your trading journal, or when explaining the strategy to others!

If you want a shorter version (e.g., for TradingView description box) or a Chinese version, just let me know — I’ll give it to you right away! 😊

200SMA Distance OscillatorThe oscillator measures the percentage deviation of closing price x from SMA200.

The idea behind the oscillator was preceded by an analysis of how often MAs in the index hold/bounce or are broken through.

Basically, the idea was about index analysis, i.e., the macro picture of a market.

Who wants to buy individual stocks when the overall market is plummeting ;-)

Or in other words: How long are you long in a market? When is it time to take profits?

After the analysis of the stability of SMAs in the index was rather modest (ratio of just under 6:4 for bounce to breakout – overall in 20, 50, 100, and 200 frames from 2020 to 2025), it was noticeable that the percentage over- or underperformance was scalable, especially in indices.

And since indices generally move upwards, there were fixed limits for over- and underestimations – especially in the longer term (SMA200) – unlike with individual stocks.

It is therefore more a question of macro trends and less of short-term movements, e.g., in day trading.

It was now interesting to see at what percentage range counter-movements were likely – particularly in the positive range for profit-taking, but of course also in the negative range for entry into sold-off markets.

If, for example, closing prices around +25% above SMA200 were reached in the NDX, the probability is very high that the market has overreacted and an interim correction will follow – so the theory goes.

On the other hand, continuous levels of +5 to +10% are a product of healthy positive development in a bull market and do not necessarily require action.

The oscillator was specifically designed for the NDX, but can also be used for the SPX and others.

The style was based on the RSI, so that the color level rises from 10% to 20% (overbought/oversold principle).

Based on manually examined movements, the criteria were set as follows:

+/-10% = flow / no color background

> +/-10% = border areas / color background

The center line represents the 252 average of the percentage deviations and could also be used as a trigger, provided it has been historically examined and is valid.

The oscillator is very interesting because it behaves completely differently from one financial instrument to another and, as a result, also in the timeframes (4h, D, W).

It would probably make sense to change the flow and border levels in the code when using it outside of indices.

The fact is that the oscillator must be “adjusted” to each instrument in order to achieve its goal of providing the best possible prediction. “Adjusting” refers to the analysis of the levels at which an instrument/asset usually reacts.

As with all indicators and oscillators, it is advisable to take other indicators and, in particular, macro news into account when analyzing this development.

If I find any substantial correlations with other indicators, I will be happy to provide an update.

The idea came from me, the code from Grok.

The code is not 100% perfect, but the data (percentage deviation, color background) is correct according to initial analysis.

In the settings, you can make the lines of the plots invisible. This makes the oscillator clearer. You can also adjust the settings for the average line.

Mars Signals - Ultimate Institutional Suite v3.0(Joker)Comprehensive Trading Manual

Mars Signals – Ultimate Institutional Suite v3.0 (Joker)

## Chapter 1 – Philosophy & System Architecture

This script is not a simple “buy/sell” indicator.

Mars Signals – UIS v3.0 (Joker) is designed as an institutional-style analytical assistant that layers several methodologies into a single, coherent framework.

The system is built on four core pillars:

1. Smart Money Concepts (SMC)

- Detection of Order Blocks (professional demand/supply zones).

- Detection of Fair Value Gaps (FVGs) (price imbalances).

2. Smart DCA Strategy

- Combination of RSI and Bollinger Bands

- Identifies statistically discounted zones for scaling into spot positions or exiting shorts.

3. Volume Profile (Visible Range Simulation)

- Distribution of volume by price, not by time.

- Identification of POC (Point of Control) and high-/low-volume areas.

4. Wyckoff Helper – Spring

- Detection of bear traps, liquidity grabs, and sharp bullish reversals.

All four pillars feed into a Confluence Engine (Scoring System).

The final output is presented in the Dashboard, with a clear, human-readable signal:

- STRONG LONG 🚀

- WEAK LONG ↗

- NEUTRAL / WAIT

- WEAK SHORT ↘

- STRONG SHORT 🩸

This allows the trader to see *how many* and *which* layers of the system support a bullish or bearish bias at any given time.

## Chapter 2 – Settings Overview

### 2.1 General & Dashboard Group

- Show Dashboard Panel (`show_dash`)

Turns the dashboard table in the corner of the chart ON/OFF.

- Show Signal Recommendation (`show_rec`)

- If enabled, the textual signal (STRONG LONG, WEAK SHORT, etc.) is displayed.

- If disabled, you only see feature status (ON/OFF) and the current price.

- Dashboard Position (`dash_pos`)

Determines where the dashboard appears on the chart:

- `Top Right`

- `Bottom Right`

- `Top Left`

### 2.2 Smart Money (SMC) Group

- Enable SMC Strategy (`show_smc`)

Globally enables or disables the Order Block and FVG logic.

- Order Block Pivot Lookback (`ob_period`)

Main parameter for detecting key pivot highs/lows (swing points).

- Default value: 5

- Concept:

A bar is considered a pivot low if its low is lower than the lows of the previous 5 and the next 5 bars.

Similarly, a pivot high has a high higher than the previous 5 and the next 5 bars.

These pivots are used as anchors for Order Blocks.

- Increasing `ob_period`:

- Fewer levels.

- But levels tend to be more significant and reliable.

- In highly volatile markets (major news, war events, FOMC, etc.),

using values 7–10 is recommended to filter out weak levels.

- Show Fair Value Gaps (`show_fvg`)

Enables/disables the drawing of FVG zones (imbalances).

- Bullish OB Color (`c_ob_bull`)

- Color of Bullish Order Blocks (Demand Zones).

- Default: semi-transparent green (transparency ≈ 80).

- Bearish OB Color (`c_ob_bear`)

- Color of Bearish Order Blocks (Supply Zones).

- Default: semi-transparent red.

- Bullish FVG Color (`c_fvg_bull`)

- Color of Bullish FVG (upward imbalance), typically yellow.

- Bearish FVG Color (`c_fvg_bear`)

- Color of Bearish FVG (downward imbalance), typically purple.

### 2.3 Smart DCA Strategy Group

- Enable DCA Zones (`show_dca`)

Enables the Smart DCA logic and visual labels.

- RSI Length (`rsi_len`)

Lookback period for RSI (default: 14).

- Shorter → more sensitive, more noise.

- Longer → fewer signals, higher reliability.

- Bollinger Bands Length (`bb_len`)

Moving average period for Bollinger Bands (default: 20).

- BB Multiplier (`bb_mult`)

Standard deviation multiplier for Bollinger Bands (default: 2.0).

- For extremely volatile markets, values like 2.5–3.0 can be used so that only extreme deviations trigger a DCA signal.

### 2.4 Volume Profile (Visible Range Sim) Group

- Show Volume Profile (`show_vp`)

Enables the simulated Volume Profile bars on the right side of the chart.

- Volume Lookback Bars (`vp_lookback`)

Number of bars used to compute the Volume Profile (default: 150).

- Higher values → broader historical context, heavier computation.

- Row Count (`vp_rows`)

Number of vertical price segments (rows) to divide the total price range into (default: 30).

- Width (%) (`vp_width`)

Relative width of each volume bar as a percentage.

In the code, bar widths are scaled relative to the row with the maximum volume.

> Technical note: Volume Profile calculations are executed only on the last bar (`barstate.islast`) to keep the script performant even on higher timeframes.

### 2.5 Wyckoff Helper Group

- Show Wyckoff Events (`show_wyc`)

Enables detection and plotting of Wyckoff Spring events.

- Volume MA Length (`vol_ma_len`)

Length of the moving average on volume.

A bar is considered to have Ultra Volume if its volume is more than 2× the volume MA.

## Chapter 3 – Smart Money Strategy (Order Blocks & FVG)

### 3.1 What Is an Order Block?

An Order Block (OB) represents the footprint of large institutional orders:

- Bullish Order Block (Demand Zone)

The last selling region (bearish candle/cluster) before a strong upward move.

- Bearish Order Block (Supply Zone)

The last buying region (bullish candle/cluster) before a strong downward move.

Institutions and large players place heavy orders in these regions. Typical price behavior:

- Price moves away from the zone.

- Later returns to the same zone to fill unfilled orders.

- Then continues the larger trend.

In the script:

- If `pl` (pivot low) forms → a Bullish OB is created.

- If `ph` (pivot high) forms → a Bearish OB is created.

The box is drawn:

- From `bar_index ` to `bar_index`.

- Between `low ` and `high `.

- `extend=extend.right` extends the OB into the future, so it acts as a dynamic support/resistance zone.

- Only the last 4 OB boxes are kept to avoid clutter.

### 3.2 Order Block Color Guide

- Semi-transparent Green (`c_ob_bull`)

- Represents a Bullish Order Block (Demand Zone).

- Interpretation: a price region with a high probability of bullish reaction.

- Semi-transparent Red (`c_ob_bear`)

- Represents a Bearish Order Block (Supply Zone).

- Interpretation: a price region with a high probability of bearish reaction.

Overlap (Multiple OBs in the Same Area)

When two or more Order Blocks overlap:

- The shared area appears visually denser/stronger.

- This suggests higher order density.

- Such zones can be treated as high-priority levels for entries, exits, and stop-loss placement.

### 3.3 Demand/Supply Logic in the Scoring Engine

is_in_demand = low <= ta.lowest(low, 20)

is_in_supply = high >= ta.highest(high, 20)

- If current price is near the lowest lows of the last 20 bars, it is considered in a Demand Zone → positive impact on score.

- If current price is near the highest highs of the last 20 bars, it is considered in a Supply Zone → negative impact on score.

This logic complements Order Blocks and helps the Dashboard distinguish whether:

- Market is currently in a statistically cheap (long-friendly) area, or

- In a statistically expensive (short-friendly) area.

### 3.4 Fair Value Gaps (FVG)

#### Concept

When the market moves aggressively:

- Some price levels are skipped and never traded.

- A gap between wicks/shadows of consecutive candles appears.

- These regions are called Fair Value Gaps (FVGs) or Imbalances.

The market generally “dislikes” imbalance and often:

- Returns to these zones in the future.

- Fills the gap (rebalance).

- Then resumes its dominant direction.

#### Implementation in the Code

Bullish FVG (Yellow)

fvg_bull_cond = show_smc and show_fvg and low > high and close > high

if fvg_bull_cond

box.new(bar_index , high , bar_index, low, ...)

Core condition:

`low > high ` → the current low is above the high of two bars ago; the space between them is an untraded gap.

Bearish FVG (Purple)

fvg_bear_cond = show_smc and show_fvg and high < low and close < low

if fvg_bear_cond

box.new(bar_index , low , bar_index, high, ...)

Core condition:

`high < low ` → the current high is below the low of two bars ago; again a price gap exists.

#### FVG Color Guide

- Transparent Yellow (`c_fvg_bull`) – Bullish FVG

Often acts like a magnet for price:

- Price tends to retrace into this zone,

- Fill the imbalance,

- And then continue higher.

- Transparent Purple (`c_fvg_bear`) – Bearish FVG

Price tends to:

- Retrace upward into the purple area,

- Fill the imbalance,

- And then resume downward movement.

#### Trading with FVGs

- FVGs are *not* standalone entry signals.

They are best used as:

- Targets (take-profit zones), or

- Reaction areas where you expect a pause or reversal.

Examples:

- If you are long, a bearish FVG above is often an excellent take-profit zone.

- If you are short, a bullish FVG below is often a good cover/exit zone.

### 3.5 Core SMC Trading Templates

#### Reversal Long

1. Price trades down into a green Order Block (Demand Zone).

2. A bullish confirmation candle (Close > Open) forms inside or just above the OB.

3. If this zone is close to or aligned with a bullish FVG (yellow), the signal is reinforced.

4. Entry:

- At the close of the confirmation candle, or

- Using a limit order near the upper boundary of the OB.

5. Stop-loss:

- Slightly below the OB.

- If the OB is broken decisively and price consolidates below it, the zone loses validity.

6. Targets:

- The next FVG,

- Or the next red Order Block (Supply Zone) above.

#### Reversal Short

The mirror scenario:

- Price rallies into a red Order Block (Supply).

- A bearish confirmation candle forms (Close < Open).

- FVG/premium structure above can act as a confluence.

- Stop-loss goes above the OB.

- Targets: lower FVGs or subsequent green OBs below.

## Chapter 4 – Smart DCA Strategy (RSI + Bollinger Bands)

### 4.1 Smart DCA Concept

- Classic DCA = buying at fixed time intervals regardless of price.

- Smart DCA = scaling in only when:

- Price is statistically cheaper than usual, and

- The market is in a clear oversold condition.

Code logic:

rsi_val = ta.rsi(close, rsi_len)

= ta.bb(close, bb_len, bb_mult)

dca_buy = show_dca and rsi_val < 30 and close < bb_lower

dca_sell = show_dca and rsi_val > 70 and close > bb_upper

Conditions:

- DCA Buy – Smart Scale-In Zone

- RSI < 30 → oversold.

- Close < lower Bollinger Band → price has broken below its typical volatility envelope.

- DCA Sell – Overbought/Distribution Zone

- RSI > 70 → overbought.

- Close > upper Bollinger Band → price is extended far above the mean.

### 4.2 Visual Representation on the Chart

- Green “DCA” Label Below Candle

- Shape: `labelup`.

- Color: lime background, white text.

- Meaning: statistically attractive level for laddered spot entries or short exits.

- Red “SELL” Label Above Candle

- Warning that the market is in an extended, overbought condition.

- Suitable for profit-taking on longs or considering short entries (with proper confluence and risk management).

- Light Green Background (`bgcolor`)

- When `dca_buy` is true, the candle background turns very light green (high transparency).

- This helps visually identify DCA Zones across the chart at a glance.

### 4.3 Practical Use in Trading

#### Spot Trading

Used to build a better average entry price:

- Every time a DCA label appears, allocate a fixed portion of capital (e.g., 2–5%).

- Combining DCA signals with:

- Green OBs (Demand Zones), and/or

- The Volume Profile POC

makes the zone structurally more important.

#### Futures Trading

- Longs

- Use DCA Buy signals as low-risk zones for opening or adding to longs when:

- Price is inside a green OB, or

- The Dashboard already leans LONG.

- Shorts

- Use DCA Sell signals as:

- Exit zones for longs, or

- Areas to initiate shorts with stops above structural highs.

## Chapter 5 – Volume Profile (Visible Range Simulation)

### 5.1 Concept

Traditional volume (histogram under the chart) shows volume over time.

Volume Profile shows volume by price level:

- At which prices has the highest trading activity occurred?

- Where did buyers and sellers agree the most (High Volume Nodes – HVNs)?

- Where did price move quickly due to low participation (Low Volume Nodes – LVNs)?

### 5.2 Implementation in the Script

Executed only when `show_vp` is enabled and on the last bar:

1. The last `vp_lookback` bars (default 150) are processed.

2. The minimum low and maximum high over this window define the price range.

3. This price range is divided into `vp_rows` segments (e.g., 30 rows).

4. For each row:

- All bars are scanned.

- If the mid-price `(high + low ) / 2` falls inside a row, that bar’s volume is added to the row total.

5. The row with the greatest volume is stored as `max_vol_idx` (the POC row).

6. For each row, a volume box is drawn on the right side of the chart.

### 5.3 Color Scheme

- Semi-transparent Orange

- The row with the maximum volume – the Point of Control (POC).

- Represents the strongest support/resistance level from a volume perspective.

- Semi-transparent Blue

- Other volume rows.

- The taller the bar → the higher the volume → the stronger the interest at that price band.

### 5.4 Trading Applications

- If price is above POC and retraces back into it:

→ POC often acts as support, suitable for long setups.

- If price is below POC and rallies into it:

→ POC often acts as resistance, suitable for short setups or profit-taking.

HVNs (Tall Blue Bars)

- Represent areas of equilibrium where the market has spent time and traded heavily.

- Price tends to consolidate here before choosing a direction.

LVNs (Short or Nearly Empty Bars)

- Represent low participation zones.

- Price often moves quickly through these areas – useful for targeting fast moves.

## Chapter 6 – Wyckoff Helper – Spring

### 6.1 Spring Concept

In the Wyckoff framework:

- A Spring is a false break of support.

- The market briefly trades below a well-defined support level, triggers stop losses,

then sharply reverses upward as institutional buyers absorb liquidity.

This movement:

- Clears out weak hands (retail sellers).

- Provides large players with liquidity to enter long positions.

- Often initiates a new uptrend.

### 6.2 Code Logic

Conditions for a Spring:

1. The current low is lower than the lowest low of the previous 50 bars

→ apparent break of a long-standing support.

2. The bar closes bullish (Close > Open)

→ the breakdown was rejected.

3. Volume is significantly elevated:

→ `volume > 2 × volume_MA` (Ultra Volume).

When all conditions are met and `show_wyc` is enabled:

- A pink diamond is plotted below the bar,

- With the label “Spring” – one of the strongest long signals in this system.

### 6.3 Trading Use

- After a valid Spring, markets frequently enter a meaningful bullish phase.

- The highest quality setups occur when:

- The Spring forms inside a green Order Block, and

- Near or on the Volume Profile POC.

Entries:

- At the close of the Spring bar, or

- On the first pullback into the mid-range of the Spring candle.

Stop-loss:

- Slightly below the Spring’s lowest point (wick low plus a small buffer).

## Chapter 7 – Confluence Engine & Dashboard

### 7.1 Scoring Logic

For each bar, the script:

1. Resets `score` to 0.

2. Adjusts the score based on different signals.

SMC Contribution

if show_smc

if is_in_demand

score += 1

if is_in_supply

score -= 1

- Being in Demand → `+1`

- Being in Supply → `-1`

DCA Contribution

if show_dca

if dca_buy

score += 2

if dca_sell

score -= 2

- DCA Buy → `+2` (strong, statistically driven long signal)

- DCA Sell → `-2`

Wyckoff Spring Contribution

if show_wyc

if wyc_spring

score += 2

- Spring → `+2` (entry of strong money)

### 7.2 Mapping Score to Dashboard Signal

- score ≥ 2 → STRONG LONG 🚀

Multiple bullish conditions aligned.

- score = 1 → WEAK LONG ↗

Some bullish bias, but only one layer clearly positive.

- score = 0 → NEUTRAL / WAIT

Rough balance between buying and selling forces; staying flat is usually preferable.

- score = -1 → WEAK SHORT ↘

Mild bearish bias, suited for cautious or short-term plays.

- score ≤ -2 → STRONG SHORT 🩸

Convergence of several bearish signals.

### 7.3 Dashboard Structure

The dashboard is a two-column table:

- Row 0

- Column 0: `"Mars Signals"` – black background, white text.

- Column 1: `"UIS v3.0"` – black background, yellow text.

- Row 1

- Column 0: `"Price:"` (light grey background).

- Column 1: current closing price (`close`) with a semi-transparent blue background.

- Row 2

- Column 0: `"SMC:"`

- Column 1:

- `"ON"` (green) if `show_smc = true`

- `"OFF"` (grey) otherwise.

- Row 3

- Column 0: `"DCA:"`

- Column 1:

- `"ON"` (green) if `show_dca = true`

- `"OFF"` (grey) otherwise.

- Row 4

- Column 0: `"Signal:"`

- Column 1: signal text (`status_txt`) with background color `status_col`

(green, red, teal, maroon, etc.)

- If `show_rec = false`, these cells are cleared.

## Chapter 8 – Visual Legend (Colors, Shapes & Actions)

For quick reading inside TradingView, the visual elements are described line by line instead of a table.

Chart Element: Green Box

Color / Shape: Transparent green rectangle

Core Meaning: Bullish Order Block (Demand Zone)

Suggested Trader Response: Look for longs, Smart DCA adds, closing or reducing shorts.

Chart Element: Red Box

Color / Shape: Transparent red rectangle

Core Meaning: Bearish Order Block (Supply Zone)

Suggested Trader Response: Look for shorts, or take profit on existing longs.

Chart Element: Yellow Area

Color / Shape: Transparent yellow zone

Core Meaning: Bullish FVG / upside imbalance

Suggested Trader Response: Short take-profit zone or expected rebalance area.

Chart Element: Purple Area

Color / Shape: Transparent purple zone

Core Meaning: Bearish FVG / downside imbalance

Suggested Trader Response: Long take-profit zone or temporary supply region.

Chart Element: Green "DCA" Label

Color / Shape: Green label with white text, plotted below the candle

Core Meaning: Smart ladder-in buy zone, DCA buy opportunity

Suggested Trader Response: Spot DCA entry, partial short exit.

Chart Element: Red "SELL" Label

Color / Shape: Red label with white text, plotted above the candle

Core Meaning: Overbought / distribution zone

Suggested Trader Response: Take profit on longs, consider initiating shorts.

Chart Element: Light Green Background (bgcolor)

Color / Shape: Very transparent light-green background behind bars

Core Meaning: Active DCA Buy zone

Suggested Trader Response: Treat as a discount zone on the chart.

Chart Element: Orange Bar on Right

Color / Shape: Transparent orange horizontal bar in the volume profile

Core Meaning: POC – price with highest traded volume

Suggested Trader Response: Strong support or resistance; key reference level.

Chart Element: Blue Bars on Right

Color / Shape: Transparent blue horizontal bars in the volume profile

Core Meaning: Other volume levels, showing high-volume and low-volume nodes

Suggested Trader Response: Use to identify balance zones (HVN) and fast-move corridors (LVN).

Chart Element: Pink "Spring" Diamond

Color / Shape: Pink diamond with white text below the candle

Core Meaning: Wyckoff Spring – liquidity grab and potential major bullish reversal

Suggested Trader Response: One of the strongest long signals in the suite; look for high-quality long setups with tight risk.

Chart Element: STRONG LONG in Dashboard

Color / Shape: Green background, white text in the Signal row

Core Meaning: Multiple bullish layers in confluence

Suggested Trader Response: Consider initiating or increasing longs with strict risk management.

Chart Element: STRONG SHORT in Dashboard

Color / Shape: Red background, white text in the Signal row

Core Meaning: Multiple bearish layers in confluence

Suggested Trader Response: Consider initiating or increasing shorts with a logical, well-placed stop.

## Chapter 9 – Timeframe-Based Trading Playbook

### 9.1 Timeframe Selection

- Scalping

- Timeframes: 1M, 5M, 15M

- Objective: fast intraday moves (minutes to a few hours).

- Recommendation: focus on SMC + Wyckoff.

Smart DCA on very low timeframes may introduce excessive noise.

- Day Trading

- Timeframes: 15M, 1H, 4H

- Provides a good balance between signal quality and frequency.

- Recommendation: use the full stack – SMC + DCA + Volume Profile + Wyckoff + Dashboard.

- Swing Trading & Position Investing

- Timeframes: Daily, Weekly

- Emphasis on Smart DCA + Volume Profile.

- SMC and Wyckoff are used mainly to fine-tune swing entries within larger trends.

### 9.2 Scenario A – Scalping Long

Example: 5-Minute Chart

1. Price is declining into a green OB (Bullish Demand).

2. A candle with a long lower wick and bullish close (Pin Bar / Rejection) forms inside the OB.

3. A Spring diamond appears below the same candle → very strong confluence.

4. The Dashboard shows at least WEAK LONG ↗, ideally STRONG LONG 🚀.

5. Entry:

- On the close of the confirmation candle, or

- On the first pullback into the mid-range of that candle.

6. Stop-loss:

- Slightly below the OB.

7. Targets:

- Nearby bearish FVG above, and/or

- The next red OB.

### 9.3 Scenario B – Day-Trading Short

Recommended Timeframes: 1H or 4H

1. The market completes a strong impulsive move upward.

2. Price enters a red Order Block (Supply).

3. In the same zone, a purple FVG appears or remains unfilled.

4. On a lower timeframe (e.g., 15M), RSI enters overbought territory and a DCA Sell signal appears.

5. The main timeframe Dashboard (1H) shows WEAK SHORT ↘ or STRONG SHORT 🩸.

Trade Plan

- Open a short near the upper boundary of the red OB.

- Place the stop above the OB or above the last swing high.

- Targets:

- A yellow FVG lower on the chart, and/or

- The next green OB (Demand) below.

### 9.4 Scenario C – Swing / Investment with Smart DCA

Timeframes: Daily / Weekly

1. On the daily or weekly chart, each time a green “DCA” label appears:

- Allocate a fixed fraction of your capital (e.g., 3–5%) to that asset.

2. Check whether this DCA zone aligns with the orange POC of the Volume Profile:

- If yes → the quality of the entry zone is significantly higher.

3. If the DCA signal sits inside a daily green OB, the probability of a medium-term bottom increases.

4. Always build the position laddered, never all-in at a single price.

Exits for investors:

- Near weekly red OBs or large purple FVG zones.

- Ideally via partial profit-taking rather than closing 100% at once.

### 9.5 Case Study 1 – BTCUSDT (15-Minute)

- Context: Price has sold off down towards 65,000 USD.

- A green OB had previously formed at that level.

- Near the lower boundary of this OB, a partially filled yellow FVG is present.

- As price returns to this region, a Spring appears.

- The Dashboard shifts from NEUTRAL / WAIT to WEAK LONG ↗.

Plan

- Enter a long near the OB low.

- Place stop below the Spring low.

- First target: a purple FVG around 66,200.

- Second (optional) target: the first red OB above that level.

### 9.6 Case Study 2 – Meme Coin (PEPE – 4H)

- After a strong pump, price enters a corrective phase.

- On the 4H chart, RSI drops below 30; price breaks below the lower Bollinger Band → a DCA label prints.

- The Volume Profile shows the POC at approximately the same level.

- The Dashboard displays STRONG LONG 🚀.

Plan

- Execute laddered buys in the combined DCA + POC zone.

- Place a protective stop below the last significant swing low.

- Target: an expected 20–30% upside move towards the next red OB or purple FVG.

## Chapter 10 – Risk Management, Psychology & Advanced Tuning

### 10.1 Risk Management

No signal, regardless of its strength, replaces risk control.

Recommendations:

- In futures, do not expose more than 1–3% of account equity to risk per trade.

- Adjust leverage to the volatility of the instrument (lower leverage for highly volatile altcoins).

- Place stop-losses in zones where the idea is clearly invalidated:

- Below/above the relevant Order Block or Spring, not randomly in the middle of the structure.

### 10.2 Market-Specific Parameter Tuning

- Calmer Markets (e.g., major FX pairs)

- `ob_period`: 3–5.

- `bb_mult`: 2.0 is usually sufficient.

- Highly Volatile Markets (Crypto, news-driven assets)

- `ob_period`: 7–10 to highlight only the most robust OBs.

- `bb_mult`: 2.5–3.0 so that only extreme deviations trigger DCA.

- `vol_ma_len`: increase (e.g., to ~30) so that Spring triggers only on truly exceptional

volume spikes.

### 10.3 Trading Psychology